TL;DR • Sex has eight key attributes, some direct in data, but mostly inferred. • Many attributes ca...

TL;DR • Sex has eight key attributes, some direct in data, but mostly inferred. • Many attributes ca...

TL;DR • Race has four/five key attributes. • Some racial attributes are easier to spot and manage th...

TL;DR • Protected attributes hide in unstructured data, proxies, and third-party sources. • Knowing ...

TL;DR • A management system standard: covers governance processes, but doesn't ensure integrity or f...

TL;DR • Narrowly applied AI definitions miss the point. • Robodebt showed us that a "simple" system ...

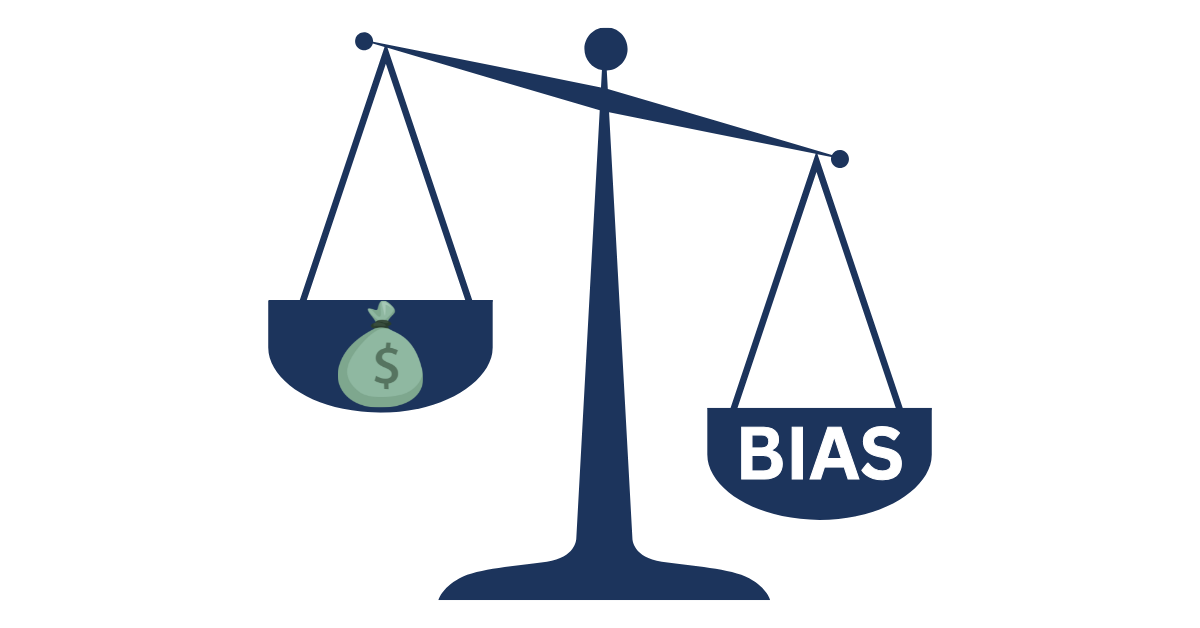

TL;DR • Preventing bias is not just about fairness. • We explore a scenario in credit card customer ...

TL;DR • Even trusted third-party tech can fail suddenly and at scale. • Generative AI providers may ...

TL;DR • Preventing bias is not just about fairness. • We explore a scenario in insurance fraud detec...

TL;DR • This featured resource is from the U.S. National Association of Insurance Commissioners • It...

TL;DR • Checklists help cover the basics and help maintain consistency. • But not everything can be ...

TL;DR • Technical stakeholders need detailed explanations. • Non-technical stakeholders need plain l...

TL;DR • Algorithmic systems create challenges in balancing explainability with privacy and confident...

TL;DR • This is a new monthly feature, with regular articles in other weeks. • This month’s research...

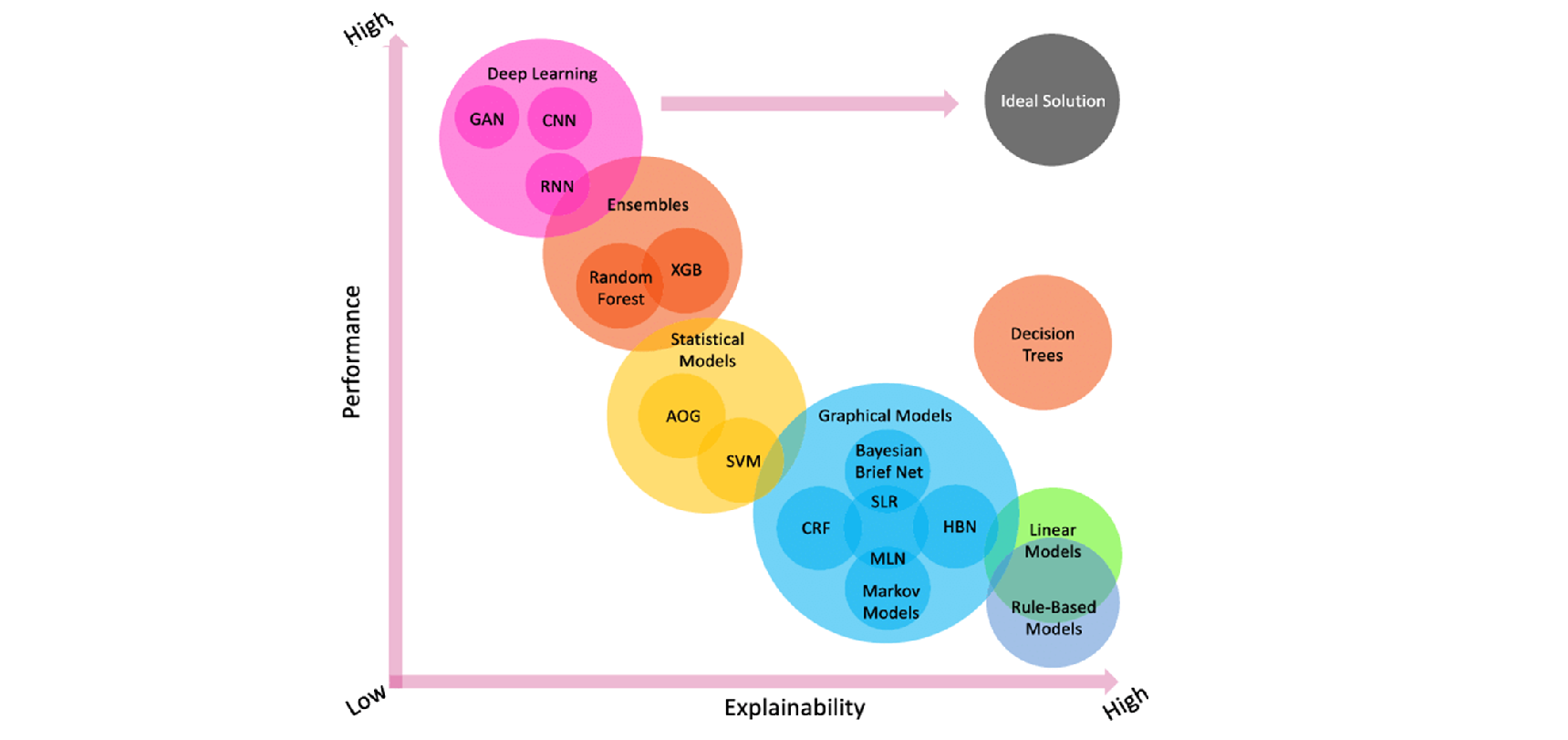

TL;DR • Explainability is necessary to build trust in AI systems. • There is no universally accepted...

TL;DR • Algorithmic processes are often complicated by intricate data flows and transformations. • D...

TL;DR • Complexity must be actively managed rather than passively accepted. • Data relevance directl...

TL;DR • Why Explainability Matters: It builds trust, is needed to meet compliance obligations, and c...

TL;DR • Testing is a core basic step for algorithmic integrity. • Testing involves various stages, f...

TL;DR • Third-party assurance for algorithm integrity varies based on the nature of the relationship...

This is the third guest interview episode of Algorithm Integrity Matters.